Knowingly or not, when we sign a mortgage contract, the loan term is almost always 30 years. That’s longer than many of the harshest criminal sentences in Australia.

The good news? You don’t have to spend a generation paying off your home and languishing in mortgage prison.

You shouldn’t let this happen to you.

Now, I say this with a slight caveat: for investors with investment debt, the situation can be different. I won’t delve into tax and financial strategies here, but often, it makes sense to stretch those out.

Let’s focus on your core owner-occupied mortgage:

1. Why not have a shorter loan-term?

2. Winning early parole through good behaviour.

3. Must do’s of refinancing.

4. Other essential strategies.

It’s a great question, and there are two main reasons we often don’t ask lenders to reduce the contracted loan term: borrowing capacity and flexibility.

Borrowing Capacity

When current and future lenders assess your borrowing capacity, they consider your contracted payments rather than your actual payments. This means that a longer loan term with lower monthly payments can enhance your borrowing potential for future loans. It doesn’t mean you’re stuck with a mortgage for the full 30 years, but it allows you more room to manoeuvre down the line.

Flexibility

Once you enter a mortgage contract, changing the terms isn’t straightforward. It typically requires a new application and a fresh credit assessment. Since life is unpredictable, it’s wise to keep your options open. By minimising your contracted repayments and maximising your actual repayments, you give yourself the greatest flexibility for any future financial needs or opportunities.

Let’s revisit that bolded line: this is the key to early release.

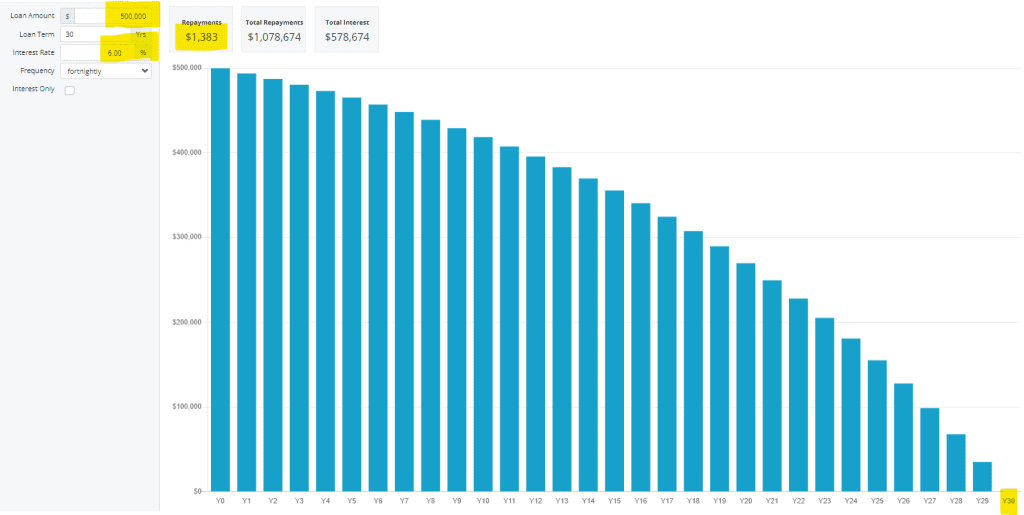

Consider this base-case example:

The blue bars represent the loan balance at the end of each year. If you take out this loan and pay it off passively, without actively managing it, you’re facing a long sentence—life without parole.

In the early years, you’ll notice the balance hardly changes. In fact, it takes 12 years to pay off the first $100,000 of your loan. That’s 40% of your loan term gone, yet you’ve only paid down 20% of the principal.

Each loan repayment consists of both principal and interest. Initially, a larger portion goes toward interest, but as the loan balance decreases, the amount allocated to principal increases. This is why the payoff curve starts flat and steepens as you progress through the loan.

Now, let’s discuss how to achieve early release:

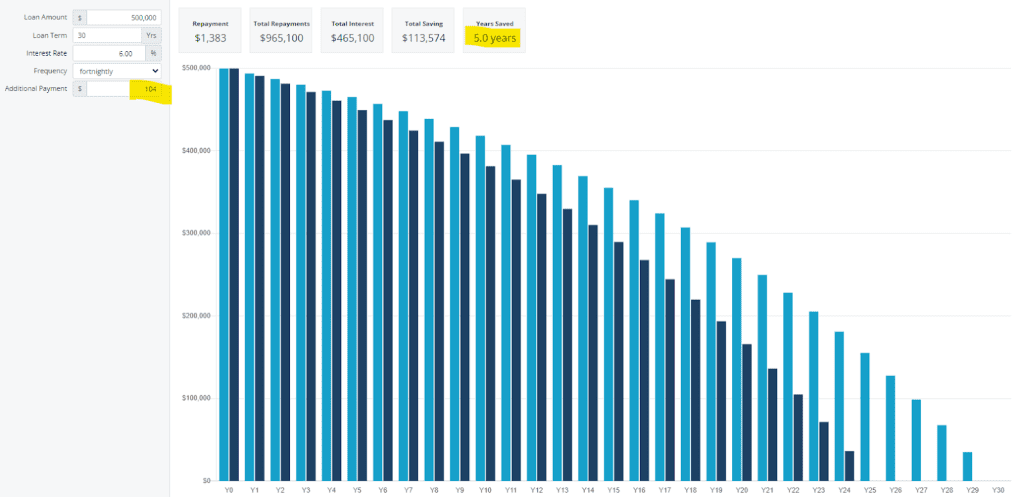

Additional Loan Repayments

The simplest strategy is to increase your actual repayments. Here’s how to cut five years off your loan term: pay an extra $104 per fortnight.

I understand that the cost of living is high, and this is easier said than done. However, you can plan for it. For example, many will see income tax cuts or pay increases in the coming months. Your future self will thank you if you can “pretend” you didn’t receive that extra income and instead direct it toward your mortgage.

Breaking It Down:

Even if you’re not a coffee drinker, consider the cost of a pot or another small treat; redirecting those funds can make a difference.

Source: ‘www.sportingglobe.com.au (with due apologies to other states where finding Carlton on tap can be a challenge—this insight comes from my limited personal market research!)

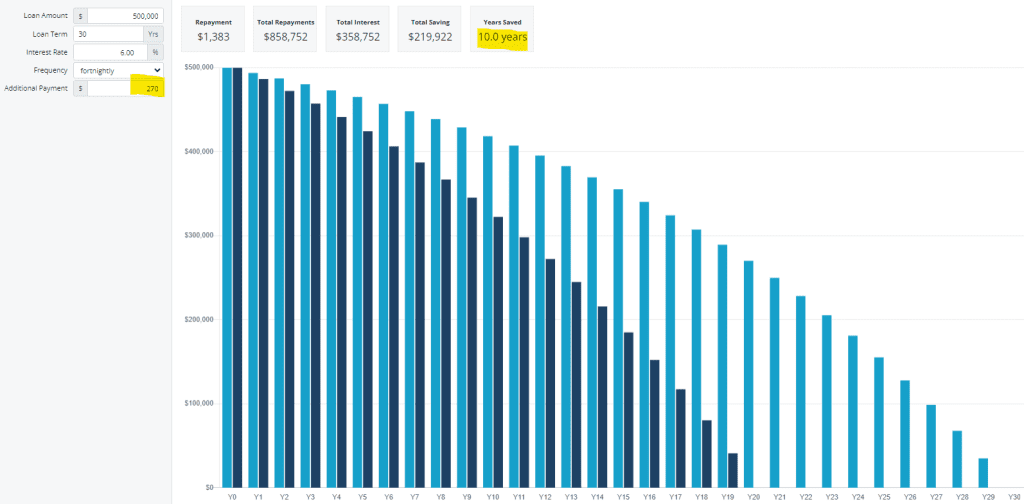

If you can commit to this strategy, consider this: paying $270 per fortnight could allow you to pay off the loan in 20 years, giving you a full decade of being mortgage-free.

Treat it as a goal—you don’t have to start at Day 1 to see significant benefits

When it comes to refinancing, there’s a common trap that’s easy to overlook, especially considering what we’ve discussed. A recent conversation with a client reminded me of this key point, which I haven’t emphasised enough.

Refinancing is a New Loan Contract

Remember, refinancing means entering a new loan contract. Just like before, this often comes with a 30-year loan term, and it’s crucial to manage it properly. If you don’t, you risk falling into a cycle of recidivism—essentially starting a new life sentence on your mortgage.

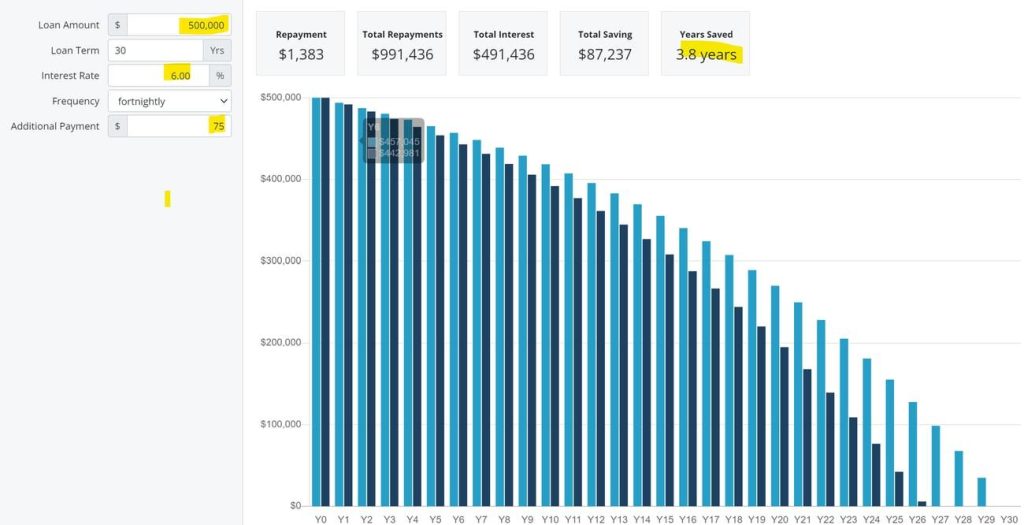

Let’s use the same loan assumptions as before:

This results in a savings of $75 per fortnight.

If you choose to put that $75 savings back into your mortgage—keeping your repayments at $1,458—you can reduce your loan term by an impressive 3.8 years.

It’s tempting to enjoy the savings, but good financial behaviour means treating this as an opportunity for extra repayments.

Why Refinancing Matters

Before you think, “What’s the use of refinancing?”, consider this: when you’re on a lower interest rate, a greater portion of any extra money you pay goes toward the principal rather than interest. This makes your payments more effective in reducing your loan term.

i. Offset Account

Make sure you have at least one offset account, and ideally three, if your lender allows. I won’t dive into the details, as everyone manages their finances differently, but here’s a quick breakdown: one account should serve as your day-to-day account, another for long-term savings, and a separate one for your emergency fund.

If you run your offset fund as your primary bank account, you could potentially reduce your mortgage payback period by years. For instance, if you maintain an average of $20,000 in your offset account, you could save approximately 2.5 years off your mortgage. Over time, that number can improve even further.

ii. Don’t Pay Off Your Mortgage

Yes, you read that correctly!

You can direct your extra repayments into your loan or into an offset account. Ideally, you should choose the latter—but only if you can commit to not touching that money. Think of it as your parole fund.

The benefits of putting money into an offset account include greater flexibility and potential tax advantages, especially if you decide to convert your home into an investment property down the line.

iii. If You Get Paid Fortnightly, Make Your Repayments Fortnightly

You’ve probably heard this advice before, often accompanied by complex explanations about how “interest is calculated daily.” While that’s true, the main benefit comes from the simple fact that there are 26 fortnightly pays in a year compared to only 12 monthly payments. This effectively means you make one extra payment toward your mortgage each year—definitely a smart move!

Please don’t feel overwhelmed by the information above.

The risk is that you might do nothing. Instead, pick one idea, plan it out, implement it, and then review your progress.

You’ll start to see your savings accumulate on your mortgage statements, and it can become quite addictive!

If you’d like to discuss your situation in more detail, just use this link to set a time that works for you: