Wow! What a week…

The global economy has been on a bit of a rollercoaster, thanks to one individual.

In the midst of all this, it’s really important to take a step back, keep a cool head, and make smart choices for ourselves.

We know things will settle eventually, and we need to plan for that.

Don’t let short-term chaos influence your long-term property decisions.

This week, we saw some well-known economists calling for an “emergency RBA meeting” this week to adjust interest rates.

My take? Let’s give it a breather! The next scheduled meeting is on May 19th, and by then, we should have a clearer picture.

As we touched on last week, everyone’s rushing to revise their interest rate forecasts, bringing them forward.

What’s driving this?

Well, you could call the “Three T’s”: tariffs (going up), trade (going down), and Trump (going where??). He is putting a lot of pressure on the Fed to cut rates.

Interestingly, lenders are already acting on updated forecasts by reducing their fixed rates.

On Friday, NAB dropped most of theirs by a significant 0.55%. That’s not just talk; it’s them putting their money where their mouth is.

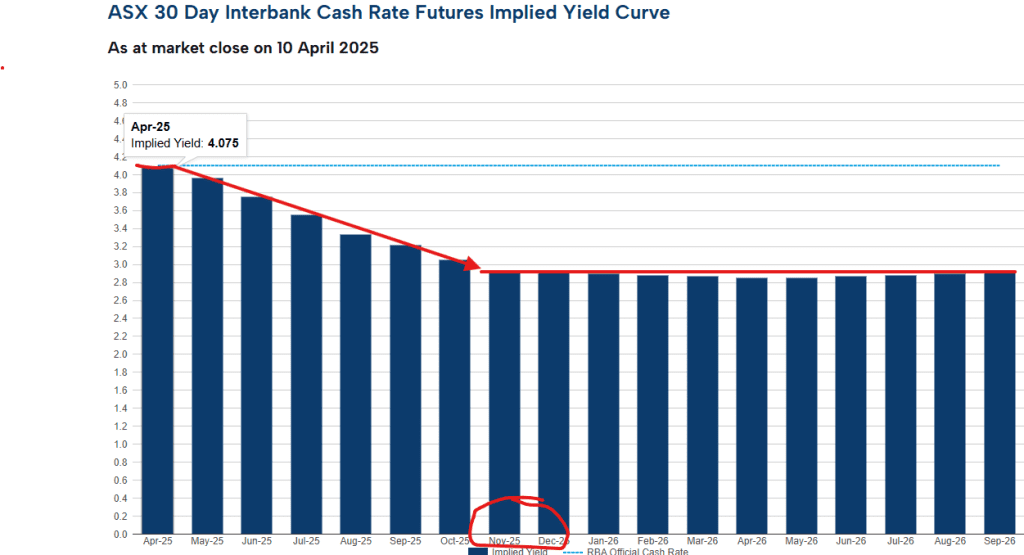

The current buzz is that the cash rate could drop to 2.85% by November. A full 1.25% lower than where we are today.

As an aside, in case you are wondering, the “floor dropping” in the title refers to the interest rate forecasts.

These are much lower than many previous forecasts.

This is the money-market consensus forecast:

Let’s dive into the impact of a potential 1% drop-in interest rates and what that could mean for you and the property market.

It’s a big topic, but let’s break it down into the main areas.

A lower cash rate generally works in three key ways:

‘1. It saves you money – a lot

1. It saves you money – a lot

For mortgage holders, this is the most immediate and obvious benefit.

For a 30-year Principal & Interest (P&I) mortgage, a 1% rate reduction would save you $63 per month for every $100,000 borrowed.

For example, with a $550,000 mortgage, that’s a saving of $348 per month (5.5 x $63). Over 30 years, that adds up to a substantial amount.

If that was to hold for 30 years you would save $125,280 off your $550k loan!!

2. You can borrow more

Depending on your situation, a 1% rate drop could increase your borrowing capacity by around 15%.

This means you will be able to afford a better property—especially important before prices potentially start to climb (see next).

It also allows many more first-home buyer to enter the market as they can now borrow more to do so.

3. Property prices should rise

Lower interest rates have two main impacts –

i. Directly, especially for owner-occupiers and particularly for first home buyers.

The above two factors are most pertinent for them just starting out.

ii. Indirectly, as lower interest rates attract more investors.

With cheaper debt, investors are willing to pay more for properties to maintain their desired returns.

For example, if an investor is borrowing 80% of a property at 6.5% interest-only, with a loan size of $800,000 their annual interest cost is $52,000. If rates drop by 1%, that cost becomes $44.000.

They could borrow an additional $200,000 or 25% more for the same cost.

Of course we should love lower interest rates!!!

My Advice:

Have a Great Week!!